Editor’s note: We have published new research and enhanced our methodology. Read our evaluation of the best HSA providers of 2022.

A good way to save for future medical expenses, like in retirement, is through a health savings account. With HSAs, pretax dollars go in, grow tax-free, and are withdrawn tax-free as long as they’re spent on qualified medical costs. It’s the most tax-advantaged savings vehicle in the tax code.

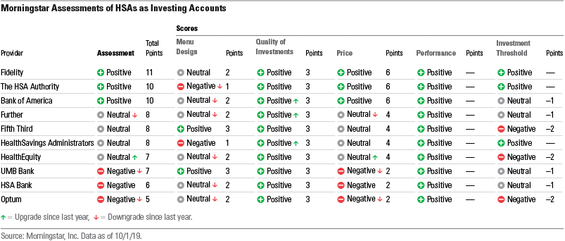

In our latest HSA study, we analyzed 10 HSA providers from an investment-account standpoint and articulated what we see as best industry practices. (Lively didn't receive an investing-account assessment because it only offers a brokerage window instead of an investment menu.)

Overall, we found that providers offer high-quality investments that have performed well. But there are significant differences between providers when it comes to fees, investment menu designs, and HSA investment thresholds (the amount investors must keep in the checking account before investing). These differences can directly impact investor outcomes, which we discuss in detail in this post.

When evaluating the best HSAs for investing, we considered five components: investment menu design, quality of investments, price, investment threshold, and performance. This is consistent with the approach we took in our prior HSA studies released in 2017 and 2018.

The best HSA for investing is in a league of its own

Fidelity emerged as the front-runner, offering the best HSA for investing. It has strong investment choices, allows people to invest the first dollar in their account, and charges low fees that no other provider can compete with. The HSA Authority and Bank of America represent the next best picks for investors. Both have good investments and cheaper fees than peers, as seen in the rankings below.

HSA fees vary across providers

We assessed providers’ prices based on total fees, which include a provider’s underlying fund fees, maintenance fees, and investment fees. Portfolios made up of passive funds are generally the cheapest options for investors, but we still found a broad range in total fees charged for a passive, well-rounded portfolio, which includes broad equity and fixed-income funds. The average HSA investor can buy a passive 60% stock/40% bond portfolio at Fidelity for an all-in cost of 0.02%, compared with 0.69% at the most expensive provider. Fidelity doesn’t charge maintenance or investment fees, so investors only have to cover the costs of the underlying funds.

Although Fidelity eschews maintenance and investment fees, most HSA providers charge maintenance fees to cover administrative costs and investment fees for the privilege of investing. Investors should consider how these fees are charged when selecting an HSA. Maintenance fees are typically dollar-based fees, whereas investment fees can be dollar-based or percentage fees levied on account assets. Percentage-based or dollar-based fees will impact investors differently depending on their account balance.

All else being equal, investors with large account balances should generally favor providers with dollar-based investment fees and avoid those with percentage-based investment fees, which can become increasingly unattractive as assets grow. Meanwhile, investors with small account balances should avoid providers with large dollar-based fees.

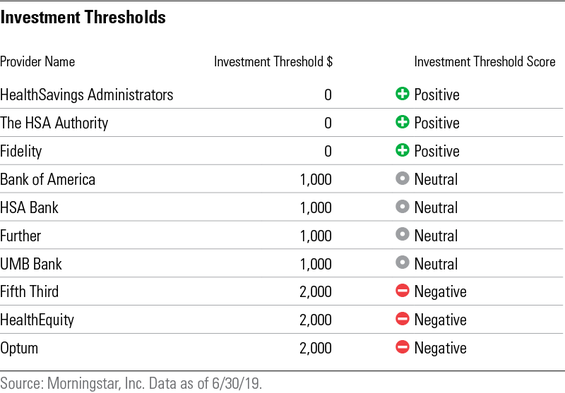

HSA investment thresholds create an opportunity cost for investors

Of the 10 providers that we analyzed, only three—HealthSavings Administrators, The HSA Authority, and Fidelity—don’t require investors to keep money in the checking account before investing. That means people who use these providers can invest all of their HSA dollars right from the start.

Like fees, investment thresholds directly impact investors’ returns because they create an opportunity cost. By holding money in a provider’s checking account, investors are missing out on higher returns they’d likely earn from investing those dollars.

In our study, the average HSA investor would miss out on 0.33% annually if they are required to keep $1,000 in the provider’s checking account. This cost doubles if they are required to keep $2,000 in the checking account—which is a material indirect expense for investors who want to shift all their HSA assets into the investment account.

Ultimately, HSA investors are better off with providers that don't have investment thresholds.

Morningstar’s best practices for HSA investment accounts

We’ve seen progress in the way that HSAs are being administered as investing accounts, though there’s still room for improvement. Here’s our view of best practices for the industry:

- Menu Design: Offer investment strategies in all core asset classes while limiting overlap among options.

- Quality of Investments: Provide strong investment strategies that earn Morningstar Medals.

- Price: Charge low fees for both active and passive strategies.

- Investment Threshold: Don’t require investors to keep money in the checking account before investing, which creates an opportunity cost.

In our next post, we’ll take a closer look at our evaluations of HSAs as spending accounts.